Don’t forget! You get access to the PRIVATE MONEY WORKSHOP REPLAY with the purchase of the Money Planner or Money Planner PDF Files. If you’ve already purchased the Money Planner, check your inbox for an invitation from the email shop@passionatepennypincher.com.

TIP: Use a pencil when you work on this one…. do as I say, not as I did! 🙂

I hope you’ve been encouraged over the last few weeks to truly rein in your finances, but today’s the day that we really are going to see the magic happen. I’ll be honest, I’ve been dreading writing this post because it’s a kind of difficult concept, but it is the one trick that REALLY will make your budget actually work.

It isn’t the easiest project, but it truly is the one thing most likely standing between you and other folks you know who have control of their finances. My husband (who, for the record, is an engineer) always knew how to do this, which has drastically impacted how we’ve managed money. I would never have learned it if he hadn’t started it way back when we were first married, but it’s like the secret sauce behind budgeting.

Are you ready for it?

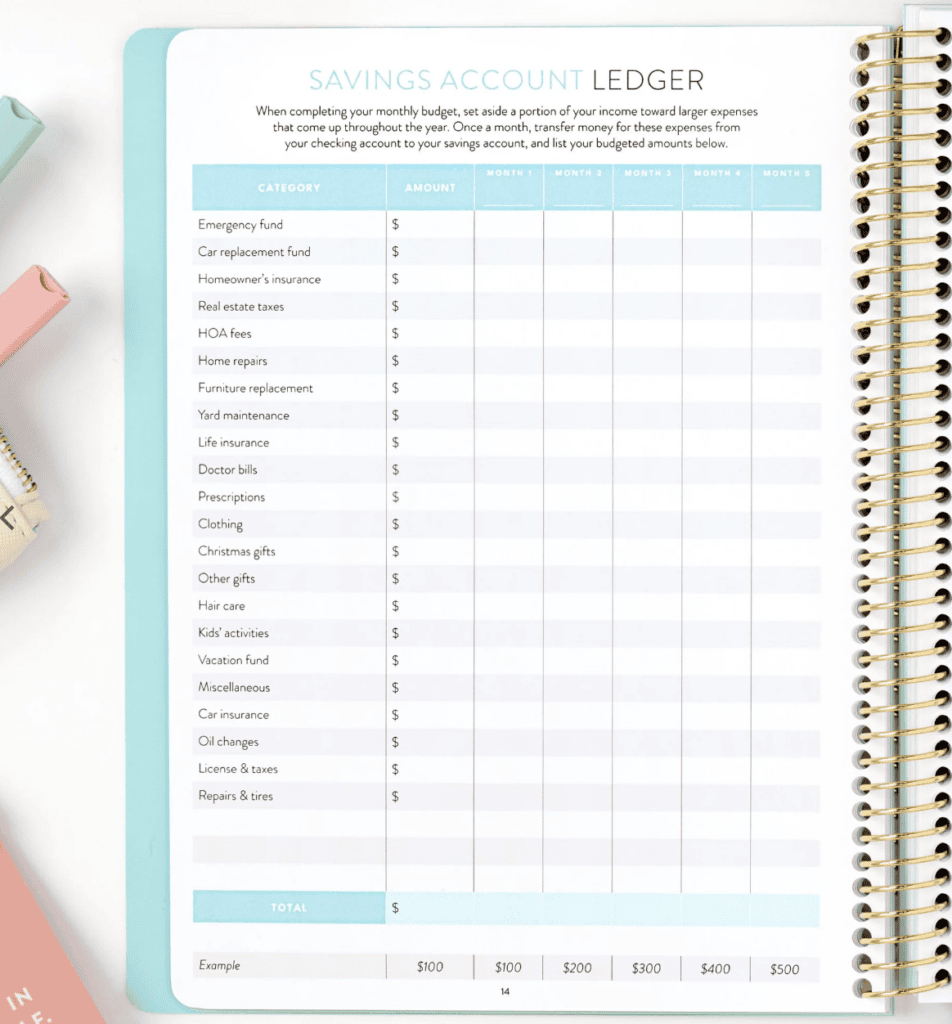

Meet the SAVINGS ACCOUNT LEDGER (found on page 14 of your Money Planner, if you have one. I recommend using a pencil as you begin, and we’re working on getting you an editable spreadsheet for this to make it go even more smoothly!) 🙂

If you’ve never heard of a savings account ledger, I promise it’s not quite as painful as it sounds. It’s simply a list that allows you to track money into categories so that you can pay larger bills that aren’t due every single month. Any item that you know will be coming at some point over the course of a year (that isn’t a regular monthly bill) would be included on your savings account ledger.

Here are a few types of budget items you might include in your savings account ledger:

- emergency fund

- car replacement fund

- homeowner’s insurance

- real estate taxes

- HOA fees

- home repairs

- furniture replacement

- yard maintenance

- life insurance

- doctor bills

- prescriptions

- clothing

- Christmas gifts

- other gifts

- hair care

- kids activities

- vacation fund

- miscellaneous

- car insurance

- oil changes

- license & taxes

- car repairs and tires

So why do you even need a savings account ledger? Well, simply put, there are things that will happen to your budget whether you plan for them or not. So you might as well plan for them, right?

You will have to pay real estate taxes at some point in the next 12 months.

You will have to pay your car insurance for the next twelve months.

Your car will most likely need service at some point in the next year, you’ll probably have to buy at least one prescription, and Christmas in December isn’t really a surprise, right?

So the savings account ledger simply allows you to write that all down on paper and then budget for that over the next 12 months.

BUT WHAT I’M ABOUT TO TELL YOU IS THE TRICK TO MAKING THIS ACTUALLY WORK. Are you ready?

You need to set up an automatic deposit into your SAVINGS account from your CHECKING account to actually make this work. Here are the exact steps.

#1 – Determine how much you need to put into each savings “category” each month.

For example, if you spend $1200 normally on Christmas gifts, take $1200 and divide it by 12 to come up with $100. EVERY SINGLE MONTH, you need to have $100 taken out of your checking account to go towards that bill so that in December, you’re not surprised that you just spent $1200.

Look back over the last year ~ how many haircuts has your family needed? If your family spends $300 a year on hair care ~ simply divide that by 12 and you’ll get $25 per month that you need to allocate for hair care each month.

#2 – Total up all of your savings account ledger accounts to come up with a total number of items you need to save for each month.

Once you’ve finished listing all of the items you need to save for each month, I want you to total that up completely so you know how much money needs to be allocated each month into a separate savings account for longer-term savings.

#3 – Set up at least one savings account at your bank, only for a monthly savings deposit towards these bigger goals.

As soon as you’ve determined how much you need to save each month, open up a savings account and have that money direct deposited as soon as your paycheck arrives. Setting this up ahead of time is the easiest way to guarantee success and will help you stick to your long-term budget goals each month.

Some folks like to have several savings accounts – possibly one for just their emergency savings, and another for more regular bills that come in throughout the year. We personally have all of ours funneled into one savings account and then pull from that as we need to pay off any specific bills.

#4 – Withdraw money from your savings account when you need to pay off one of the bills listed in these accounts.

In the wintertime, you won’t likely need to spend any money on yard care, but in May or June, you might need to have a service spray your yard for weeds. That money will sit in your savings account throughout the year so that it’s available when you need it. When you take it out, deduct it from your savings account ledger and rebuild the account each month.

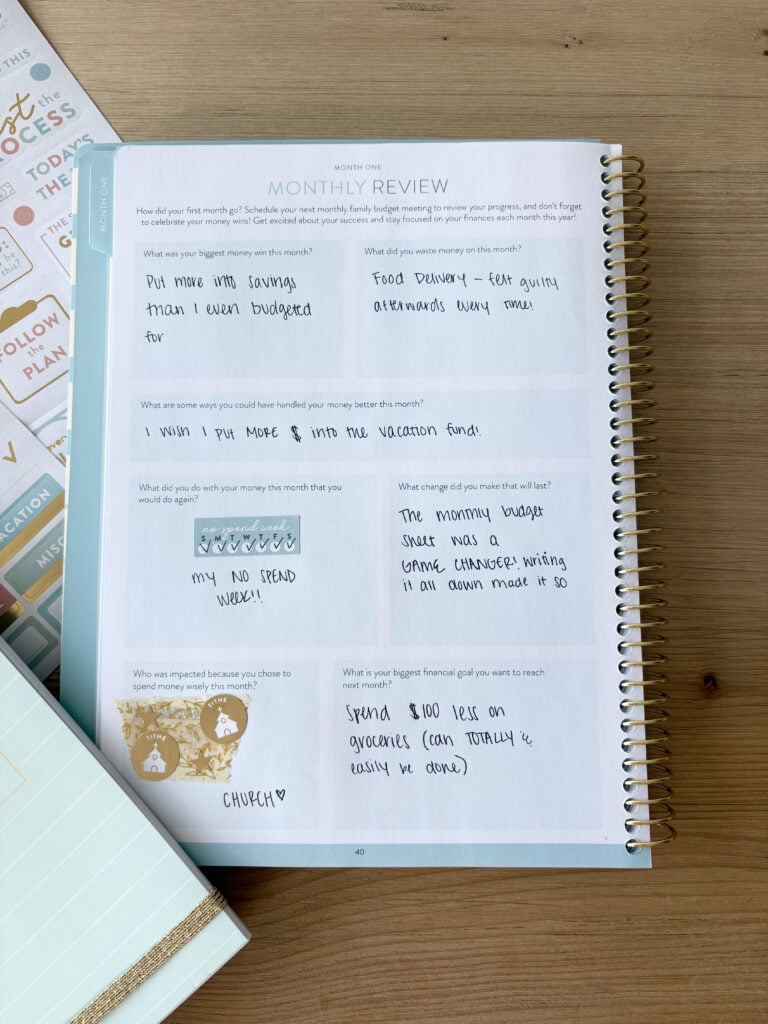

#5 – At least once a year, re-evaluate your savings account ledger to make sure you’re allocating the right amount to each category.

Are you spending way more on home repairs than you thought but not as much on clothing? Would you like to save more for your vacation fund but not quite as much on new furniture? Did you get a raise or lose a job, which means you need to adjust the total amount you’re putting into savings? Make sure those amounts are working for you!

ONE BIG SIDE NOTE to all of this:

LIFE HAPPENS AND USUALLY ISN’T SUPER NEAT AND TIDY.

An emergency will happen. Your license and tax fees might surprise you and go way up one year. If you have to “borrow” money from what you’ve saved for doctor bills to cover an unexpected water leak, it is okay and you are so much better off than if you hadn’t created a longer-term savings account to start with.

And, once you’re to the point of financial freedom, you may not need to hold this list quite so tightly. For our own family, my husband religiously updated this list every single month for probably the first fifteen to twenty years in our marriage. Now, we have a set amount that stays in our savings account so we know we can cover any unexpected bills that arise, which is such crazy freedom and I so want that for you.

But when we were starting out, we had to figure out a system that would work, and this is the one that worked for us. I’m betting it will work if you’re new to budgeting and just starting out now, too.

Your turn now!

What do YOU budget for each month? DO you even budget for longer-term, larger categories in your budget? Do you keep a separate amount in savings for things like this?

Leave a comment to share and let me know ~ I sure do love hearing from you!

New to budgeting and don’t know where to start? We’re in the middle of our Finance February Money Challenge, and it’s a great time to hop on board and transform your finances today!

- Creating a Monthly Budget Worksheet

- The 2026 Money Planner is Here! Fix Your Finances Forever

- 5 Steps To Budgeting (On An Irregular Income)

- How to Create A Debt Reduction Plan

- How to Create a Bill Payment Schedule That Works for You

- Top Grocery Budget Busters

Do you use a budget planner manually or digital?I would like to use however you do it.

I personally use the budget planner manually. I like to have things spread out in front of me so I can see everything. Can’t wait to hear what works for you!